Only an Accident: Courts Judge Fatal Colonoscopy Not Worthy of Payout

Previous stories in William Heisel's "Only an Accident" series include:

Only an Accident: Fatal Colonoscopy Leaves Family Stunned and Unpaid

Only an Accident: Insurance Claim Denied After Fatal Colonoscopy

When in college and heading home for Christmas break one winter, I hit a patch of icy road. I pumped my breaks – as every good Montana driver confronted with ice knows to do – attempted to steer into the snow along the shoulder and, instead, slid off the road and through a barbed wire fence. Praise be to the farmer who erected that fence because it kept me from sliding even further into a water-filled ravine.

I had insurance. And I had an AAA card. So I got a tow and had a claim agent size up the damage. His ruling: It was an accident.

There are always things you can do to lessen the chances of an accident, but the fact that accidents can and do happen is the central reason why people buy car insurance, homeowner’s insurance, and life insurance.

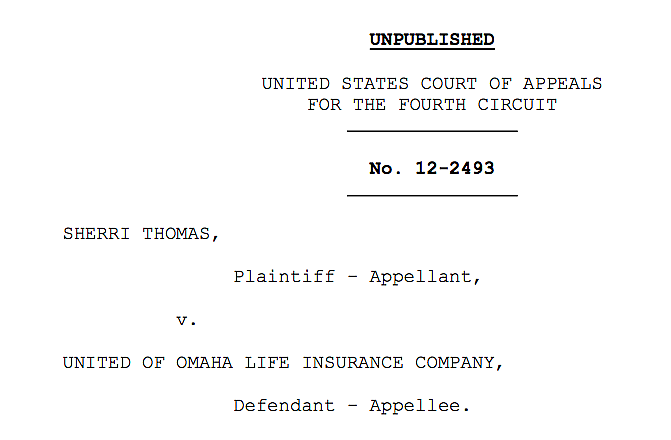

United of Omaha Life Insurance Company – a subsidiary of Mutual of Omaha – has turned that central reason for buying insurance inside out by deciding that accidents aren’t accidents at all if they happened in a medical setting. The company’s decision has been affirmed by the U.S. District Court for Maryland and then affirmed again by the U.S. Court of Appeals for the Fourth Circuit.

The rulings have broad implications for patients and their families. I explained how Middleton died last week and how the insurance company deliberated on Friday. Now here’s a bit about what went into the judges’ thinking.

First, the evidence. According to the appeals court ruling, the courts reviewed the following:

(1) the amended death certificate for Plaintiff’s husband, issued by the State of Maryland

(2) the Post Mortem Examination Report prepared by Assistant Medical Examiner Victor Weedn, M.D., for the Office of the Chief Medical Examiner for the State of Maryland

(3) the private autopsy report prepared by Allen Burke, M.D.

(4) Middleton’s medical records from the Montgomery Endoscopy Center where he underwent the colonoscopy

(5) the professional opinion of United of Omaha’s Medical Director, Thomas Reeder, M.D., regarding the cause of Middleton’s death, following his review of the claim file.

The appeals court paid special attention to Weedn’s report, noting:

Of particular relevance to the present appeal, Dr. Weedn’s Report states that Middleton, at the time of his death, was on a liver transplant list, and that he underwent the colonoscopy as part of his workup for an anticipated liver transplant due to a family history of colon cancer. Dr. Weedn learned this information from his first-hand review of Middleton’s medical records, including records from: (1) Shady Grove Adventist Hospital (emergency services); (2) Dr. Mikhail (primary care physician); (3) Dr. David Doman (the gastroenterologist who performed the colonoscopy at issue); (4) Dr. Mark Sulkowski (infectious disease, internal medicine); and (5) Dr. Alan Kravitz (surgeon). According to Dr. Weedn’s Report, “[t]he manner of [Middleton’s] death is ACCIDENT.”

Middleton’s policy with United of Omaha defined an accident narrowly as an unexpected event that had to occur “independent of Sickness and all other causes.”

One’s mind reels as to how an accident could occur without any cause. Perhaps Middleton’s widow, Sherri Thomas, should have sued on the grounds of misrepresentation. Under what circumstances, exactly, would an accidental death benefit be paid if the insurance company already had ruled out any accidents in which there was a cause involved?

But the courts stepped around this issue and focused on the “independent of Sickness” part. Was Middleton sick at the time of the accident? From his death certificate, it appears so. He suffered from cirrhosis and hepatitis C. Was the colonoscopy, and, therefore, the accident related to his sickness? Therein lies the difficulty. Thomas and her attorneys argued that Middleton was undergoing a colonoscopy as a precautionary measure – not because of his liver disease. He had a family history of colon cancer and had undergone two previous colonoscopies over a decade.

Three judges considered the evidence for the appeals court: J. Harvie Wilkinson III, G. Steven Agee and Clyde H. Hamilton. They wrote:

In conclusion, we hold United of Omaha did not abuse its discretion in denying Plaintiff’s claim for accidental death benefits under the Policy with respect to the death of her husband. Accordingly, the district court did not err in granting summary judgment in favor of United of Omaha.

“Alice in Wonderland,” right? And the only Cheshire Cat grinning is the CEO of Mutual of Omaha. Sell accidental death insurance with no possibility of collecting. That’s a winning business strategy, and it’s also a cautionary tale for anyone considering undergoing what they think might be a routine procedure. If illness can cancel out an insurance policy, than we may all reconsider why we are paying those premiums, as most of us suffer from some sort of illness. At a minimum, we should read the fine print of our policies.

Part 1: Fatal Colonoscopy Leaves Family Stunned and Unpaid

Part 2: Insurance company says, Tough luck, accidents happen

Photo by Jeroen Bouman via Wikimedia Commons.

{kind=link}